Most people have no idea what they’re actually paying for in healthcare. Between surprise bills, hidden facility fees, and insurance processing charges, the final cost often bears no resemblance to the initial estimate.

At NuMed DPC, we believe transparent healthcare costs should be the standard, not the exception. Our direct primary care model strips away the financial opacity that defines traditional insurance-based medicine, giving you clear visibility into every dollar you spend on your health.

Where Does Your Healthcare Dollar Actually Go?

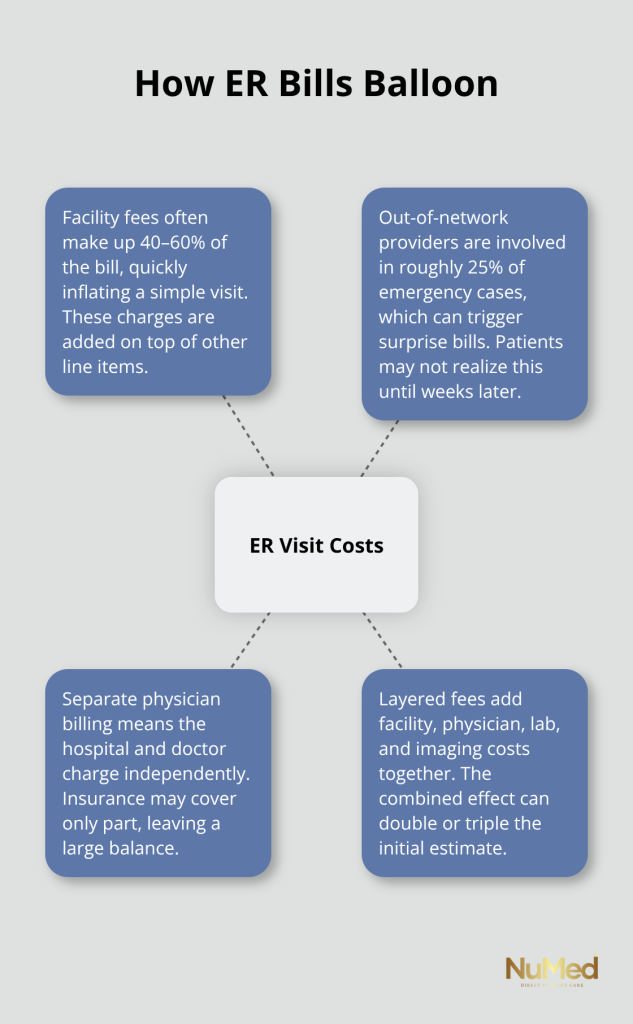

The average American family spends between $12,000 and $15,000 annually on healthcare, yet most have no clear understanding of what they’re actually paying for. Emergency room visits illustrate this problem starkly. A simple ER visit for a minor injury costs $1,500 to $3,000, with facility fees alone accounting for 40 to 60 percent of the bill. Hospitals charge facility fees on top of physician fees, lab fees, and imaging fees-a layering effect that inflates costs rapidly.

When an ER visit involves an out-of-network provider (which occurs in roughly 25 percent of emergency cases), you face surprise bills weeks or months later. The physician bills separately from the hospital, and your insurance covers only a portion, leaving you liable for thousands in unexpected charges.

Administrative overhead adds another layer of cost that patients rarely see. Insurance companies employ thousands of people to process claims, deny coverage, and handle appeals. Hospitals and physician offices mirror this burden, with staff spending roughly 40 percent of their time on insurance-related paperwork rather than patient care. That administrative waste gets passed directly to you through higher premiums, higher deductibles, and higher out-of-pocket costs at the point of service.

The Deductible Trap

High-deductible health plans have become standard. This means you pay full price for most primary care visits until you hit your deductible, at which point insurance coverage finally begins. A routine office visit costs $150 to $250 out of pocket before your deductible applies. Add annual physicals, preventive lab work, and urgent care visits, and many families never fully benefit from their insurance coverage. The system penalizes you for seeking care early, which contradicts how healthcare should work.

Why Pricing Remains Hidden

Healthcare pricing operates across multiple invisible tiers. Hospitals maintain chargemaster prices that list astronomical amounts, but insurers negotiate secret discounts that patients never see. Cash-pay patients often face the highest prices. If you call a hospital to ask the cost of an MRI, you receive vague answers because the price depends entirely on your insurance plan, or lack thereof. This opacity exists by design. Without clear pricing, patients cannot shop for care or make informed decisions about their health spending, which benefits hospitals and insurers far more than it benefits you.

This pricing confusion sets the stage for understanding how a different model, one built on transparency from the ground up, can fundamentally change your relationship with healthcare costs.

How Direct Primary Care Strips Away Financial Opacity

The direct primary care model operates on a principle that traditional insurance deliberately avoids: complete price transparency. A flat monthly membership fee, typically between $50 and $100 for adults depending on age and services, covers primary care visits of 30 to 60 minutes, with no copays, no deductibles, and no surprise bills waiting in your mailbox. This single monthly payment actually covers your care instead of sitting as a deductible you must exhaust before coverage begins. According to 2024 data from the American Academy of Family Physicians, DPC monthly fees range from $20 to $50 for children and $50 to $100 for adults, making the cost structure predictable and manageable for household budgeting.

Labs and Services Cost Substantially Less

In the DPC model, lab work and imaging are either included in your membership or offered at substantially discounted rates compared to hospital chargemaster prices. A standard blood panel costs $25 to $75 through negotiated rates. An EKG that hospitals bill at $150 to $300 costs $25 to $50. Ultrasounds drop from $400 to $800 down to $150 to $300. This pricing advantage exists because the insurance middleman disappears entirely. No claims processing, no authorization requests, no appeals process. The administrative staff that traditionally spends 40 percent of their time on insurance paperwork can focus on actual patient care instead. This efficiency translates directly to lower service costs. When you need labs, you schedule them, receive results within days, and get a clear invoice with no mystery charges appearing months later.

Administrative Waste Vanishes

The traditional healthcare system wastes approximately $300 billion annually on administrative overhead, according to research from Harvard Medical School. Hospitals employ entire departments to fight with insurance companies over coverage denials. Physician offices hire billing specialists whose sole job is to manage the insurance approval process. Patients spend hours on the phone with insurers trying to understand what is actually covered. In a DPC practice, this entire layer of bureaucracy disappears. No one denies your claim. No one sends you a bill six months later because a code was entered incorrectly. No one argues with your insurance about whether your visit was medically necessary. Care providers simply deliver care and bill you directly. Studies show that DPC practices operate with administrative costs of roughly 10 to 15 percent compared to traditional practices at 40 percent or higher. That difference means more money spent on actual healthcare and less spent on paperwork.

Minor Procedures Stay Affordable

In-office procedures-skin biopsies, suture removal, EKGs, and similar services-cost significantly less in a DPC setting because the administrative overhead that inflates hospital pricing no longer applies. You avoid facility fees, authorization delays, and the markup that hospitals add to every service. The direct relationship between patient and provider eliminates the financial intermediaries that traditionally inflate costs at every step.

Understanding how DPC eliminates these hidden expenses reveals why the total cost of care differs so dramatically from traditional insurance. Preventive care through DPC practices significantly reduces hospital admissions, further lowering overall healthcare spending. The next section examines exactly how much families actually save when they switch from high-deductible plans to transparent, membership-based primary care.

What Your Family Actually Spends on Healthcare

A family of four with employer-sponsored insurance faces a healthcare cost structure that bears little resemblance to the advertised premium. Annual premiums for employer-sponsored family health coverage reached $26,993 this year, but that’s only the beginning. Once you add the deductible, copays, and out-of-pocket maximums that typically reach $8,000 to $15,000 per person, the true annual cost climbs to $30,000 to $45,000 for many families. In contrast, that same family switching to DPC pays a flat monthly membership of $75 per adult and $35 per child, totaling roughly $2,640 annually for primary care without any deductible, copay, or surprise bills. The math becomes clearer when you add preventive care benefits. Traditional insurance penalizes early care-seeking because you must exhaust your deductible before coverage applies. A family making three preventive visits annually at $150 to $250 per visit out of pocket pays $450 to $750 before insurance even begins covering expenses. In a DPC model, those same visits cost nothing beyond the monthly membership. Labs included in or discounted through DPC memberships save an additional $400 to $800 annually compared to hospital pricing, since routine blood work costs $100 to $150 per panel through traditional insurance versus $25 to $75 through DPC negotiated rates.

Chronic Disease Management Transforms Your Bottom Line

For families managing chronic conditions like diabetes or hypertension, the savings accelerate dramatically. A patient with diabetes visits their doctor monthly for medication adjustments and lab monitoring, spending $600 to $1,200 annually in copays alone under traditional insurance, not counting the labs themselves. The same patient in a DPC practice with unlimited visits and included or discounted labs pays their monthly membership fee and nothing more, eliminating the financial barrier to frequent check-ins that actually prevent complications. A 60-year-old managing three chronic conditions through monthly DPC visits and continuous medication optimization avoids the emergency department visits that plague patients in traditional insurance systems who cannot afford regular monitoring. That patient’s total healthcare spending drops to $8,000 to $12,000 annually, including all primary care, labs, and medications, compared to $25,000 to $40,000 in traditional insurance that includes premiums, deductibles, copays, and emergency care costs that preventive monitoring would have avoided entirely.

Early Detection Prevents Expensive Emergencies

The financial advantage of DPC extends far beyond primary care costs because preventive care fundamentally changes how disease progresses. A patient diagnosed with hypertension during a routine annual physical in a DPC setting can start treatment immediately and receive monthly follow-up visits at no additional cost, preventing the stroke or heart attack that costs $500,000 to $1,000,000 in hospital care. Traditional insurance discourages this preventive approach because patients avoid doctor visits due to copays and deductibles, meaning conditions like uncontrolled blood pressure, undiagnosed diabetes, and high cholesterol go undetected until emergencies force expensive hospitalizations. Research shows that preventive care saves significantly in downstream emergency and hospital costs.

A DPC patient catching early-stage kidney disease through annual lab work starts dialysis prevention strategies immediately, while a traditional insurance patient delaying care due to cost avoidance faces eventual dialysis at $40,000 to $60,000 annually. A 45-year-old patient with a family history of heart disease receives an EKG for $25 to $50 in a DPC practice during a comprehensive annual visit, identifying a previously unknown arrhythmia that gets managed with medication. That same patient in traditional insurance may skip the EKG due to cost concerns and experience a heart attack five years later, resulting in $100,000 to $200,000 in acute care costs plus ongoing cardiac rehabilitation expenses.

Long-Term Savings Accumulate Significantly

Over a decade, families practicing preventive care through DPC accumulate savings of $15,000 to $30,000 in avoided emergency department visits, urgent care visits, and hospitalizations compared to families in traditional insurance who delay care due to financial barriers. The most significant savings emerge for patients over 55, where chronic disease prevalence peaks. A patient catching early-stage kidney disease through annual lab work starts dialysis prevention strategies immediately, while a traditional insurance patient delaying care due to cost avoidance faces eventual dialysis at $40,000 to $60,000 annually. The financial cascade matters significantly when you compare outcomes across different healthcare models. Patients who access preventive care consistently experience fewer hospitalizations, shorter hospital stays when they do occur, and lower medication costs due to early intervention and disease management.

Final Thoughts

Healthcare costs should never remain a mystery. The financial opacity that defines traditional insurance-based medicine creates barriers to care, discourages preventive treatment, and leaves families vulnerable to surprise bills that arrive months after a single visit. Transparent healthcare costs represent more than just clarity on pricing-they fundamentally change how you approach your health and your financial security.

We at NuMed DPC built our practice around the principle that you deserve to know exactly what you pay for and why. Our direct primary care model eliminates the hidden fees, administrative waste, and surprise billing that plague traditional insurance. A flat monthly membership covers your primary care visits, labs, and services without copays, deductibles, or unexpected charges. When preventive care becomes affordable and accessible, you catch diseases early, avoid expensive emergency department visits, and manage chronic conditions before they escalate into hospitalizations.

Taking control of your healthcare future means rejecting the system that profits from your confusion and choosing transparency instead. Experience compassionate and holistic healthcare with NuMed DPC, where we focus on preventing illness by addressing root causes and fostering a personalized connection between you and your practitioner. Our extensive lab services, functional medicine, and health coaching are tailored to your unique needs without insurance hassles or hidden costs.